Weekly Recap

February 24, 2025

Crypto Fundamentals #103

Fundamentals matter for crypto to be real.

.webp)

Jon Ma

Co-Founder / CEO

Fundamentals matter for crypto to be real.

Hey Artemis Analysts,

Jon here from Artemis. I’m a former software analyst who studied fundamentals for a living and believe fundamentals will matter more for crypto in order for the world’s economy and financial system to move onchain.

We had an interesting last week with:

I’ll be writing weekly recaps on what’s happening in digital finance each week.

There’s been a shift on Crypto Twitter towards analyst highlighting real businesses and business performance aka “Make Fundamentals Great Again”.

Jeff Dorman, the CIO at Arca, responded to one of our comp tables with leading DeFi protocols by looking at the MC/Revenue comps of Coinbase and Robinhood which just had their earnings in the month:

True to our TradFi roots, we put together a comp table comparing multiples of leading DeFi vs leading fintechs companies.

The market has had quite the draw down in the last week or so but it was interesting to see leading DeFi with fundamentals and leading fintechs somewhat converge in multiples — DeFi with 7.1x MC/Revenue and Fintechs with 8.7x MC/Revenue

It’s worth noting that there’s a pretty big gap between DEXs / aggregators like Raydium, Aerodrome, Jupiter which trade at 2.4-2.7x and say a Hyperliquid which trades at 11.8x and is a L1 and leader in perp DEXs with various other product lines.

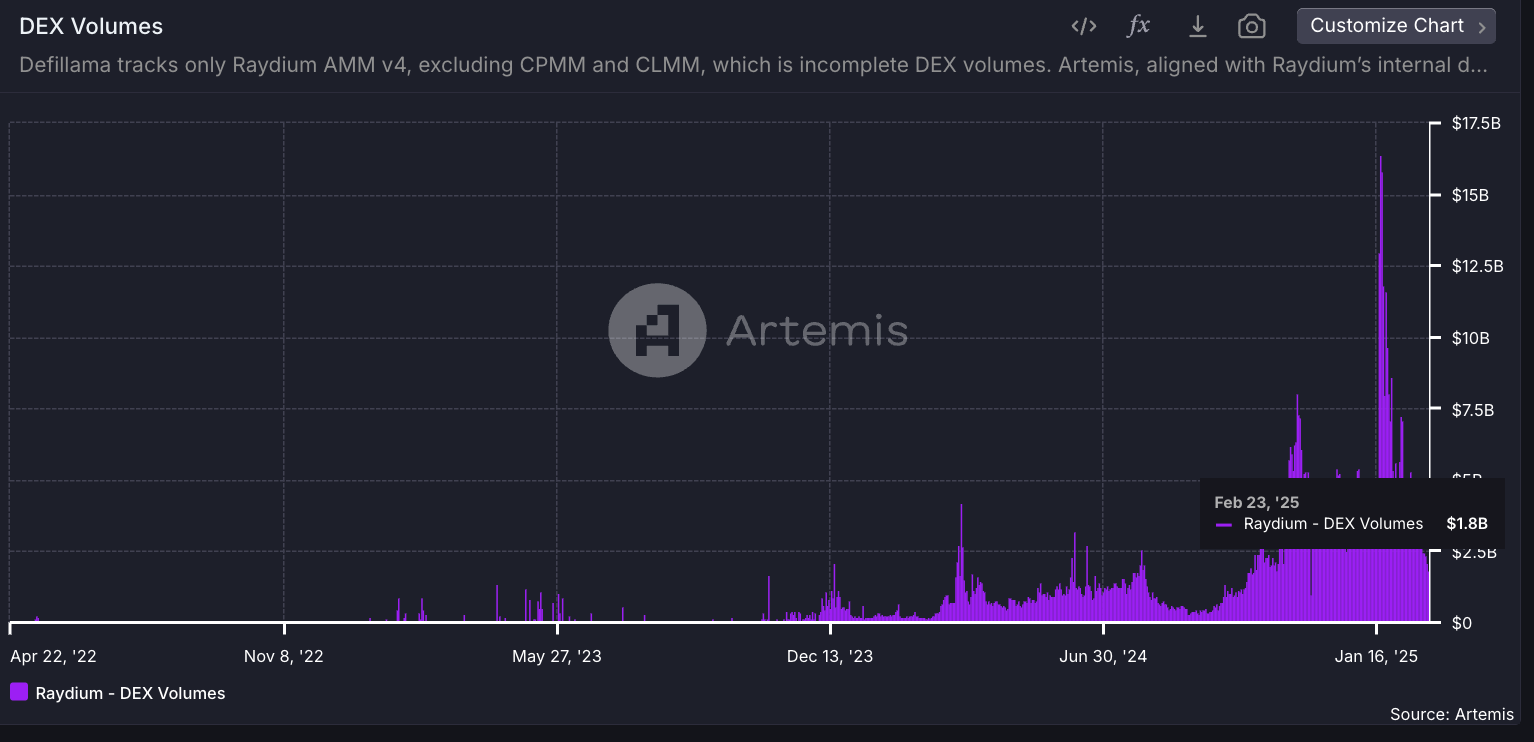

The crypto market does react to fundamentals: today it was reported Pump.fun launched their own AMM liquidity pool where tokens would graduate to pump.fun pools instead of Raydium’s.

This matter a lot for Raydium since 20-30% of Raydium’s volumes come from Pump.Fun. Raydium is down 28% as investors worry about the reduction in DEX volume and hence fees and potential revenue buyback.

The main question crypto projects will face is what is the floor in terms of multiple and how sticky is the revenue?

Who is the buyer of last resort if a protocol trades for 1x revenue? If meme coin volumes continue or is replaced by other volume like other digital asset swaps, foreign currency swaps or even tokenized equity swaps, these multiples could be quite reasonable and, in hindsight, low in the long term.

On the multiple side of things, in the SaaS world, SaaS multiples more or less trade at 6-7x ARR.

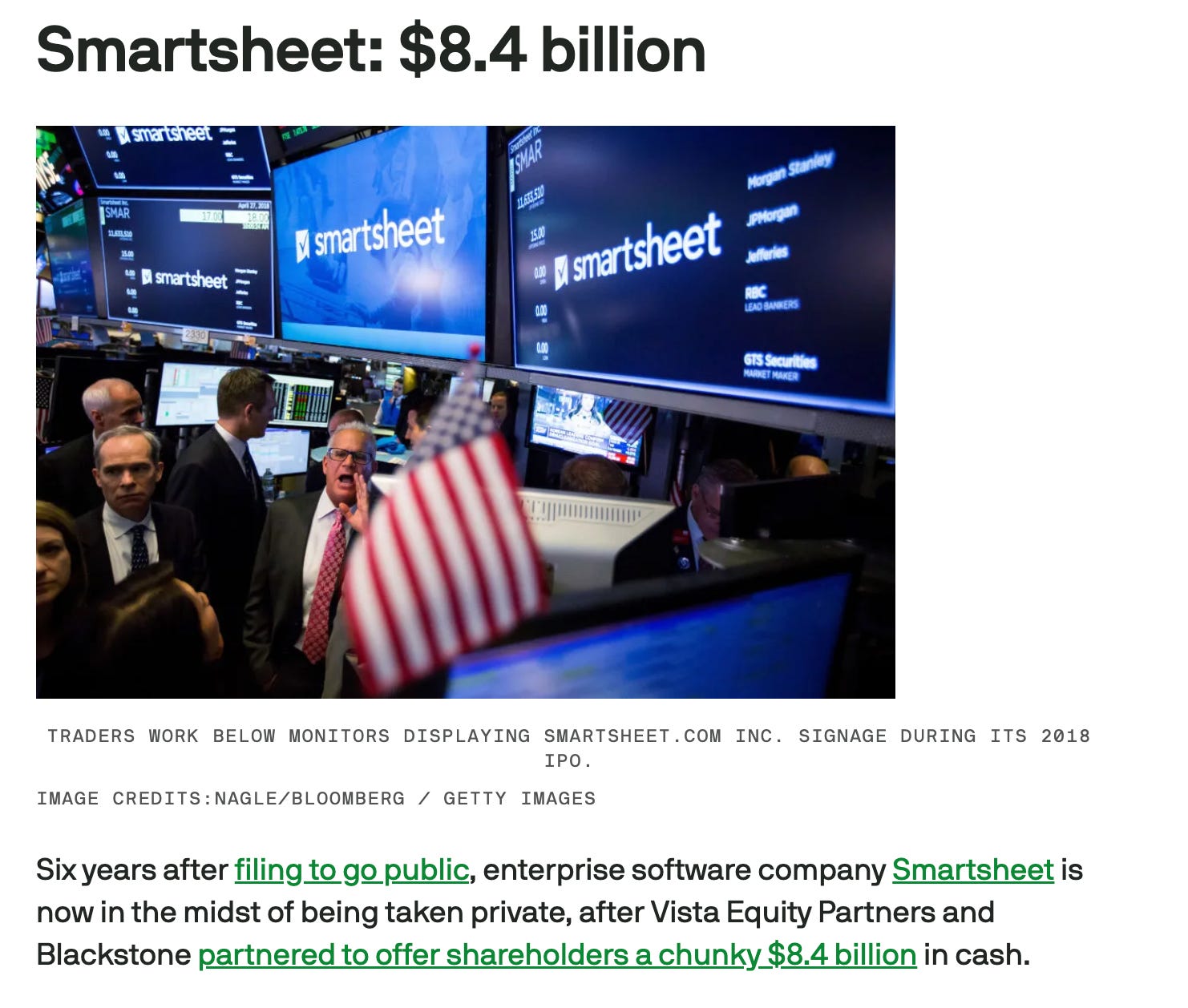

Below a certain multiple, Private Equity firms like Blackstone, Thoma Bravo, Vista would come in and take these public companies private if they become incredibly attractive from an ARR and FCF multiple perspective

In 2024, we had 14 take-private transactions of software businesses—Smartsheet, for example, was acquired at 6.5x ARR, in line with industry comps

We’re of the camp that multiples for fintechs and DeFi protocols will converge overtime especially as DeFi protocols become “onchain fintechs” and mass amounts of users move onchain. But we believe we’ll need to large asset managers who see the value of protocol revenue buybacks or potential “private equity” like institutions buying large amounts of governance tokens in order to influence protocols.

We look forward to continuing our coverage of the fintech/crypto multiple convergence.

Crypto markets sank overall back to ~$3T due to concerns around Trump tariffs and trade wars alongside the pump and dump of the $LIBRA token.

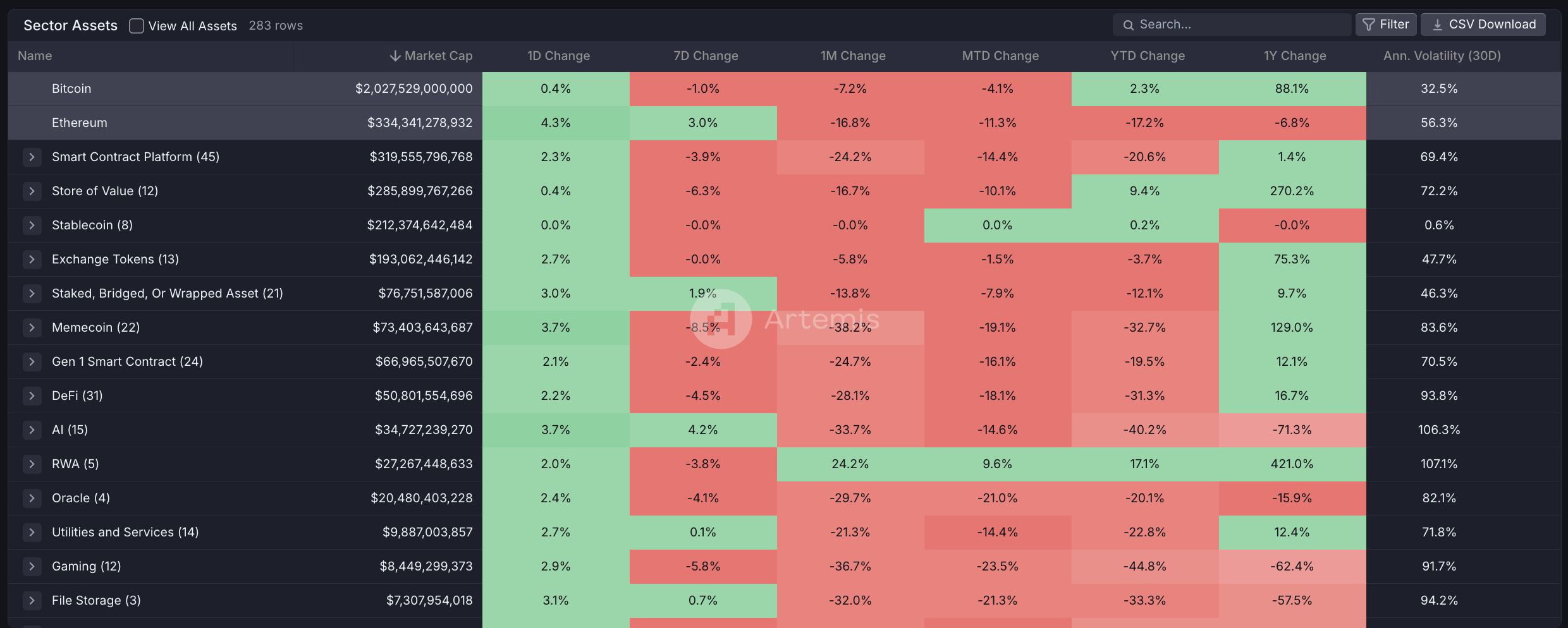

Our colleague Crystal highlighted crypto sector performance

We pointed out that RWAs have outperformed primarily in the last month driven by Plume, a RWA focused public blockchain.

Our belief that market drawdowns aren’t necessarily a bad thing as the market shifts back towards projects with real fundamentals and real world use cases.

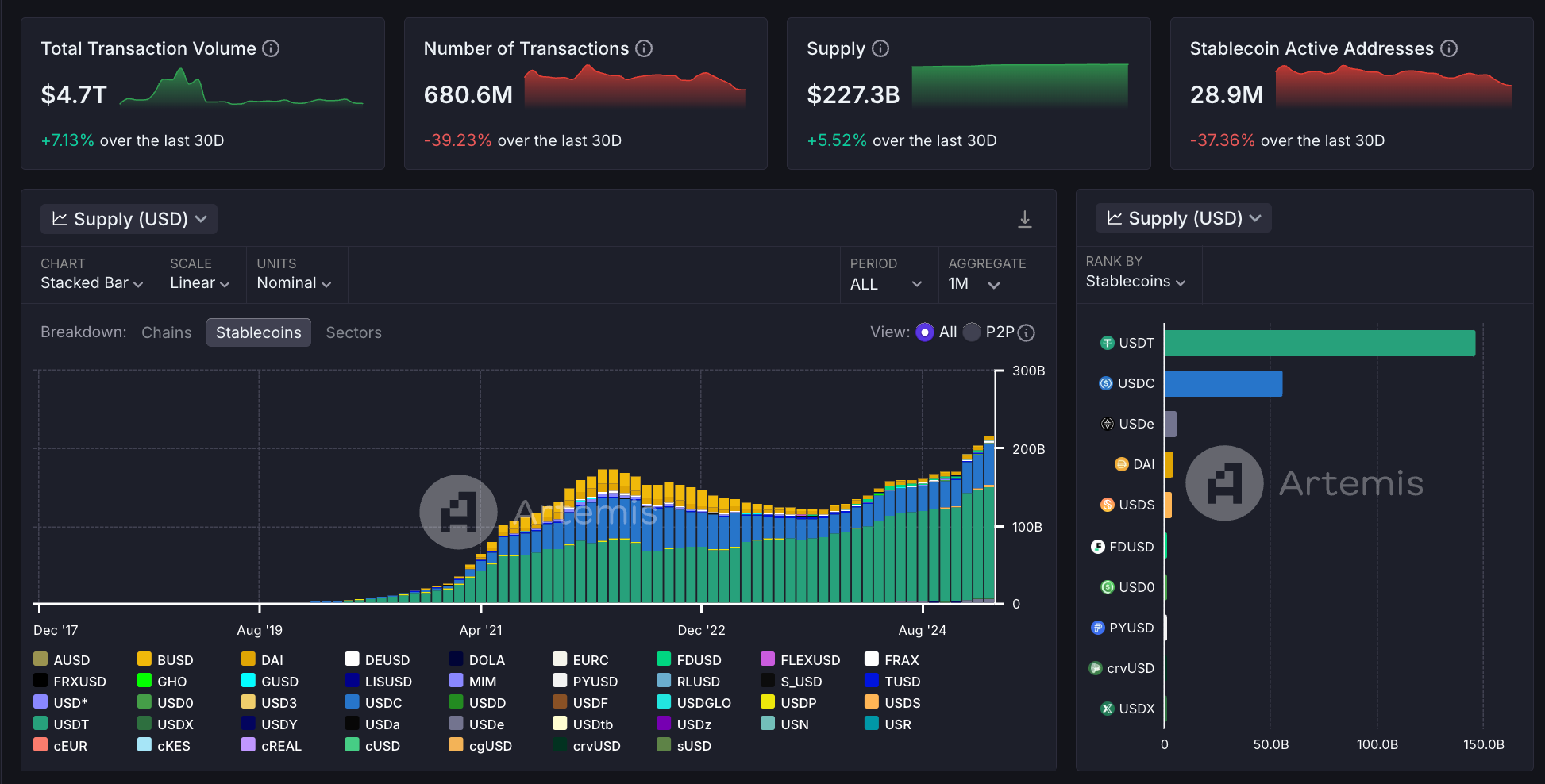

Despite FUD and criticism of crypto for only enabling memecoin and degenerate gambling, stablecoins continue to grow and get adopted globally.

Stablecoin supply grew to $227B which is an all-time high.

It’s without a doubt that stablecoins are clearly a killer use case of blockchains — the founders of Stripe (the largest fintech in the world) were on the all-in podcast talking about use cases like Scale AI paying international contractors seamlessly versus traditional payment rails.

We also recently updated our stablecoin marketmap and highlighted 3 companies in particular:

$KAITO went live this past Thursday and the token is sitting at $1.6B FDV as of the writing (which is much greater than the $400-$600m FDV range analyst thought KAITO would launch at)

Just when the market thought the “AI” narrative around blockchains were dead, Kaito became the best performing AI token.

A few interesting pieces about the $KAITO launch:

A line that I particularly appreciated from Yu Hu, their founder/CEO: “ultimately, we believe fundamentals matter, and our product determines our value. we’re grateful that kaito - an application, not an L1, not a (typical) exchange, with a new concept and no real comps - is seeing support from the market”

Yano at Blockworks had a great take: the mold of raising seed, Series A, Series B, etc is changing and “all equity will get tokenized”.

Our core thesis of digital finance is that EVERYTHING will move onchain and public equities, private equity (e.g private companies and startups) will all move onchain, allowing anyone access to world class companies and equities.

It’s worth pointing out that day 1 $KAITO was listed on Binance and Coinbase, some of the largest centralized exchanges in the world, thereby allowing any investor in the world access to the asset.

We’re interested to see if more crypto companies and non-crypto companies (e.g private B2B SaaS or AI companies) follow a similar route to launching a token versus the traditional IPO route.

Happy Monday,

Jon

Subscribe to our newsletter and understand what’s happening on-chain.